12 / 56

12 / 56

As we look at the panoramic

view of the year for 2014 —

year over year — we con-

tinue to see all the ways the

vacation ownership industry

is rebuilding and growing key

revenue lines once more.

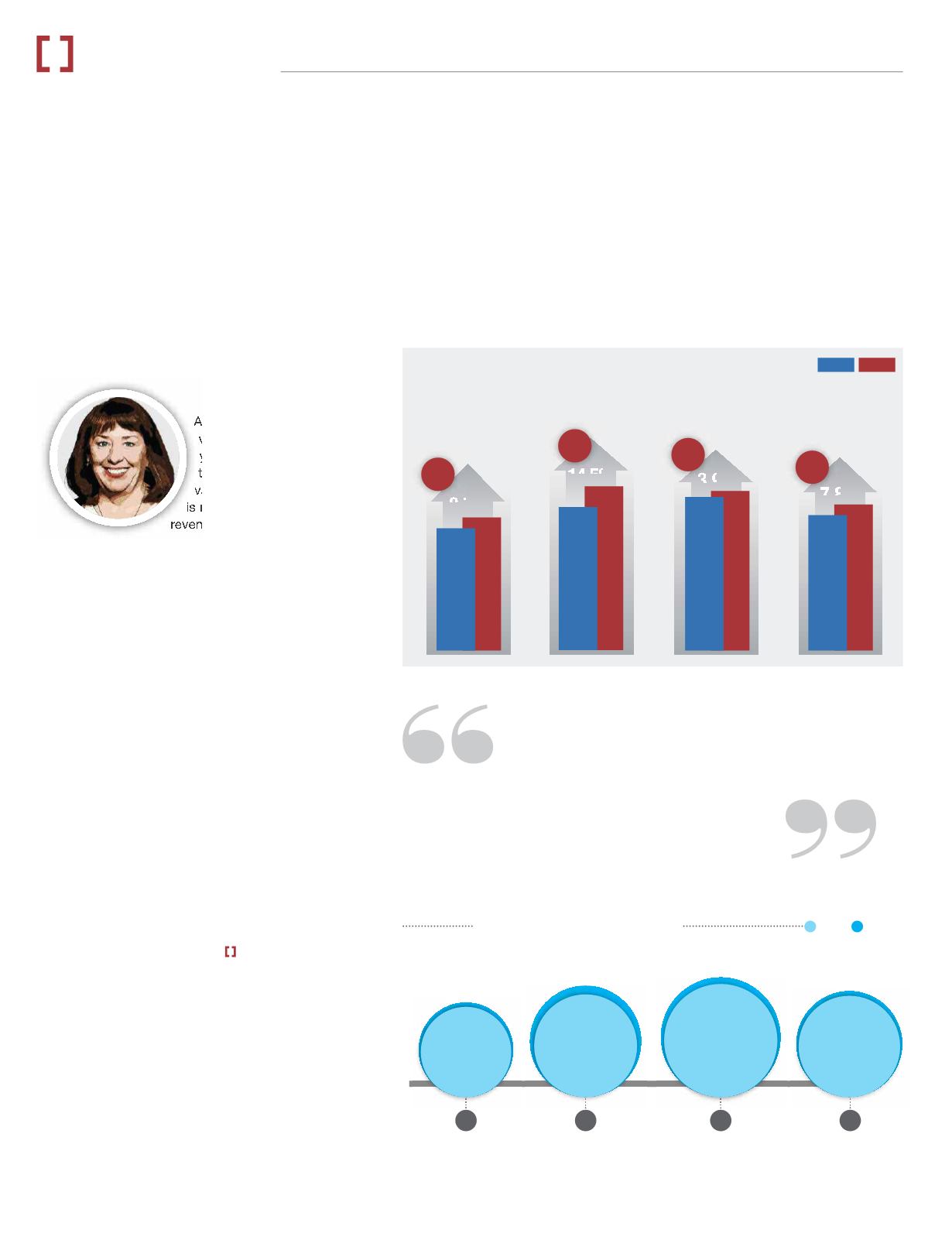

Sales Performance

Using the lens of the four quarterly pulse surveys

prepared for the ARDA International Foundation

(AIF) by Deloitte & Touche LLP in 2014, here are

some of the strongest performance indicators

pointing the way to the resurgence.

Unpacking the Data

There’s an overall increase of tours that is driving

up sales across the board. And along with those

good-news points, we are seeing that volume per

guest (VPG) rates are also down for two of the

four quarters (Q2 & Q3).The fluctuation in VPG

coupled with the overall increase in tours may

suggest that the industry is working on bringing in

more new buyers vs. repeated buyers.

This movement into the market of first-time

owners indicates the kind of progress we like to

see for vacation ownership across the board, as

the upcoming release of the 2015

State of the

Vacation Ownership Industry

report will only

underscore. All of this bodes well for sustainable

growth in new markets and going beyond our

loyal existing owner base.

Darla S. Zanini, RRP, is executive vice president of

the ARDA International Foundation (AIF).

10

IN BRIEF

RESORTDEVELOPER.COM

vacation industry review

JULY – SEPTEMBER 2015

Pointing the Way to Growth

AIF Quarterly Surveys Show Continued

Climb in Timeshare Sales

Sales Performance

2014 pulse report

Net-originated timeshare sales (including telesales & fee-for-service):

US$1.230 billion

US$1.340 billion

US$1.467 billion

US$1.680 billion

US$1.593 billion

US$1.655 billion

US$1.515 billion

2013 2014

8.7%

14.5%

3.9%

7.8%

Q1

Q4

Q3

Q2

TOURS ARE UP

2013 2014

By Darla S. Zanini

Q1

The fluctuation in VPG coupled with the

overall increase in tours may suggest that

the industry is working on

bringing in

more new buyers vs. repeat buyers

.

Q2

Q3

Q4

US$1.634 billion

Source: Deloitte & Touche

483,730

639,374

593,469

548,455

500,201

627,965

667,293

564,475